With shifting interest-rate expectations, record home equity, and evolving borrower behavior, 2026 is shaping up to be a surprising year for mortgage refinancing. This in-depth guide explores seven shocking refinance trends, real-life homeowner examples, and expert insights to help you decide whether refinancing now could save you money—or cost you more in the long run.

For many homeowners, refinancing has felt like a missed opportunity. Those who didn’t lock in ultra-low rates years ago often assume the window is closed. But that assumption is increasingly outdated.

As 2026 approaches, refinancing conversations are shifting. Instead of asking “Are rates low enough?”, homeowners are asking deeper, more strategic questions about cash flow, flexibility, and long-term financial stability.

According to projections from the Mortgage Bankers Association (MBA), refinance activity is expected to rebound meaningfully in 2026 after several slow years. This rebound isn’t driven by one dramatic rate cut—it’s driven by a combination of economic, behavioral, and lending-market changes that most homeowners haven’t fully connected yet.

This article breaks down seven shocking refinance trends for 2026, explains how real homeowners are using them, and helps you decide whether now is the right time for you to refinance—or whether waiting could be smarter.

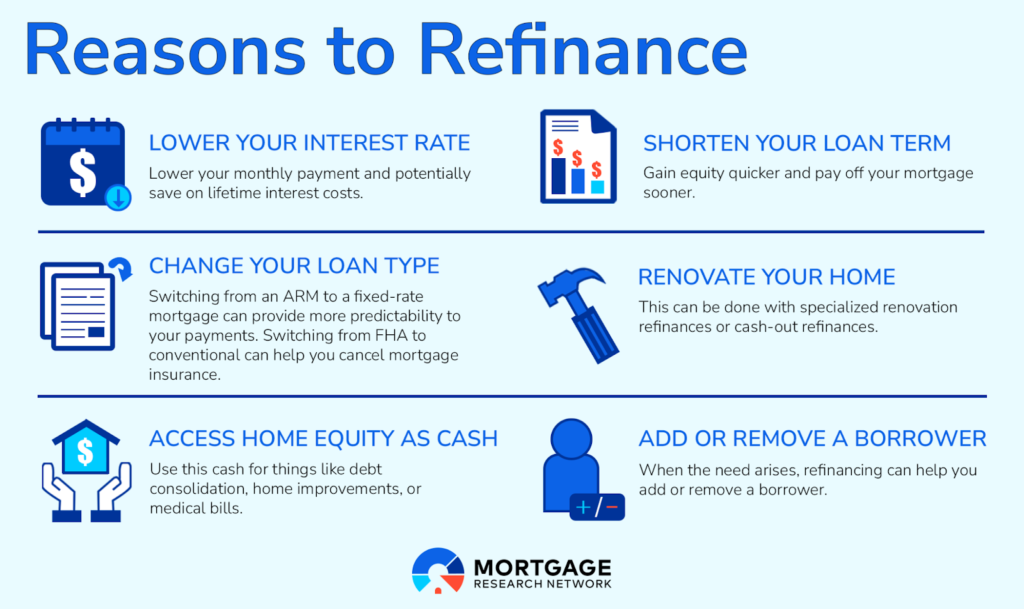

For years, refinancing was almost synonymous with chasing the lowest interest rate. That mindset no longer tells the full story.

In 2026, homeowners are refinancing to:

- Reduce monthly financial pressure

- Remove mortgage insurance

- Rebalance debt

- Tap equity without selling

- Adjust loan terms to match life stages

Refinancing has become a strategic financial tool, not just a reaction to rate changes.

One of the biggest myths still circulating is that refinancing only works if rates fall by at least one full percentage point. In 2026, that belief is quietly costing homeowners money.

Many refinances are succeeding because they:

- Remove PMI

- Extend or shorten loan terms

- Improve cash flow

- Eliminate higher-risk loan structures

Mark bought his home in 2022 at a 6.9% interest rate. In early 2026, rates were only modestly lower. Still, refinancing allowed him to eliminate PMI and slightly restructure his loan—cutting his monthly payment by $230. Over five years, that savings added up significantly.

The total monthly obligation matters more than the headline rate.

Despite economic uncertainty, U.S. homeowners are sitting on historic levels of equity.

According to CoreLogic, the average homeowner with a mortgage enters 2026 with nearly $290,000 in equity. This equity is creating refinancing opportunities even in a higher-rate environment.

Homeowners are using equity to:

- Pay off high-interest debt

- Fund essential home upgrades

- Create financial buffers

- Avoid selling and repurchasing in expensive markets

Angela refinanced to consolidate $34,000 in credit card debt into her mortgage. Even with a similar rate, her monthly expenses dropped by over $650—relieving constant financial stress.

For years, 30-year mortgages dominated the market. In 2026, many homeowners are intentionally moving toward 20-year or 15-year loans.

Why the shift?

- Faster equity growth

- Massive long-term interest savings

- Earlier financial freedom

A dual-income couple in Utah refinanced from a 30-year loan to a 20-year loan. Their payment rose slightly, but they cut nearly $140,000 in lifetime interest and positioned themselves to be mortgage-free before retirement.

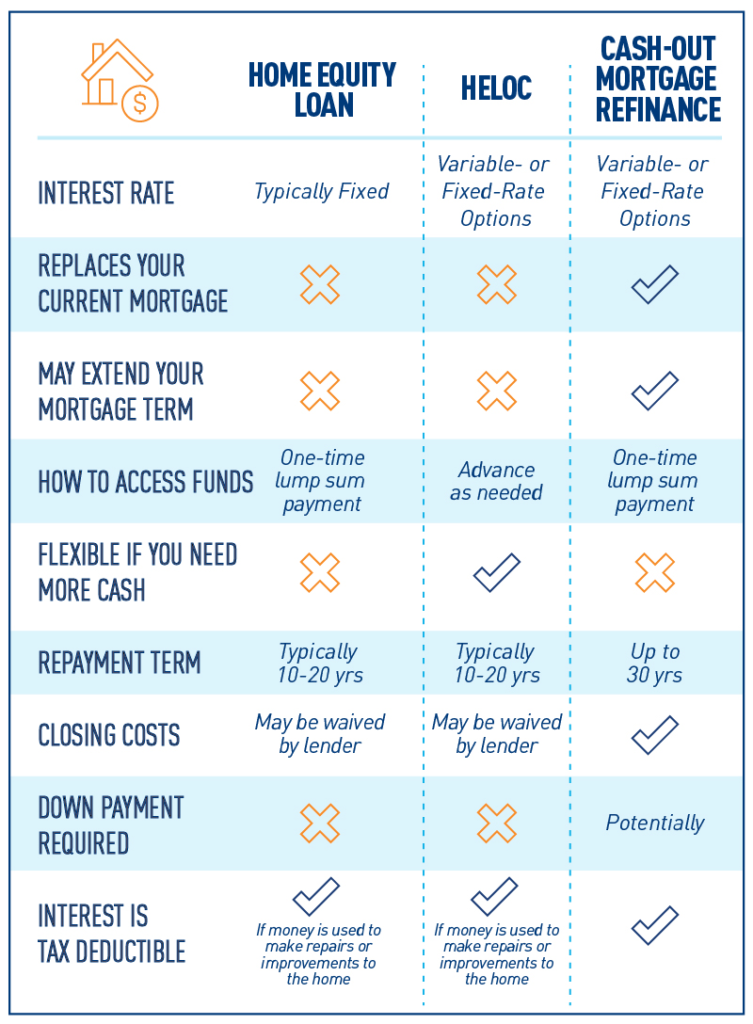

Cash-out refinances once had a reputation for fueling overspending. In 2026, usage patterns look very different.

Homeowners are increasingly using cash-out refinances for:

- Energy-efficient improvements

- Home expansions instead of moving

- Medical or education costs

- Strategic investing

Instead of upgrading to a more expensive home, Robert refinanced and used equity to add living space. The refinance was cheaper than moving and avoided higher purchase prices.

Cash-out refinancing should strengthen your balance sheet—not weaken it.

Private Mortgage Insurance (PMI) is often overlooked—but it’s a powerful refinance trigger.

Many homeowners who put less than 20% down now exceed that threshold due to:

- Market appreciation

- Principal reduction

Yet PMI doesn’t always fall off automatically, especially with FHA loans.

Emily refinanced solely to remove PMI. Her closing costs were recovered in under two years, and she saved over $10,000 long-term.

With purchase activity fluctuating, lenders are targeting refinance borrowers with strong profiles.

Borrowers with:

- Solid credit

- Stable income

- Significant equity

are seeing:

- Lower fees

- Faster processing

- More flexible structures

This competition gives qualified homeowners more leverage in 2026 than in recent years.

Perhaps the biggest trend isn’t economic—it’s psychological.

Homeowners are no longer waiting for headlines to announce “the best time to refinance.” Instead, they’re asking:

- Does this reduce stress?

- Does this improve cash flow?

- Does this align with my life plans?

The answer is increasingly personal, not market-driven.

Refinancing may be smart if:

- You plan to stay in your home for several years

- You can reduce monthly costs

- You want to remove PMI

- You’re consolidating high-interest debt

- You’re restructuring your loan strategically

Refinancing may not make sense if:

- You plan to sell soon

- Closing costs outweigh benefits

- You’re increasing debt unnecessarily

- Your income is unstable

- Rates aren’t the only factor

- Equity creates flexibility

- Loan structure matters

- Personal timing beats market timing

- The best refinance improves quality of life

1. Is 2026 a good year to refinance a mortgage?

Ans. For many homeowners, yes—especially those with strong equity, stable income, or PMI they want to remove.

2. Do interest rates need to drop a lot to refinance?

Ans. No. Refinancing can make sense through PMI removal, term changes, or debt consolidation.

3. How much equity do I need to refinance in 2026?

Ans. Most lenders prefer at least 20% equity, though some programs allow less.

4. Is cash-out refinancing risky?

Ans. It can be if misused, but strategic cash-out refinances can improve financial stability.

5. Can refinancing lower monthly payments without a lower rate?

Ans. Yes. Removing PMI or adjusting loan terms can reduce payments even with similar rates.

6. How long do I need to stay in my home for refinancing to be worth it?

Ans. Typically 2–5 years, depending on closing costs and monthly savings.

7. Does refinancing reset my mortgage term?

Ans. Often yes, unless you choose a shorter loan term like a 15- or 20-year mortgage.

8. Are lenders more flexible with refinancing in 2026?

Ans. Many lenders are competing harder for qualified refinance borrowers.

9. Can I refinance an FHA loan into a conventional loan?

Ans. Yes, and many homeowners do this to eliminate lifelong FHA mortgage insurance.

10. What’s the biggest refinancing mistake homeowners make?

Ans. Focusing only on interest rates instead of total financial impact.

Refinancing in 2026 isn’t about predicting interest-rate headlines—it’s about aligning your mortgage with your life.

Homeowners who benefit the most aren’t chasing the market. They’re analyzing their numbers, goals, and stress levels honestly.

If refinancing improves your cash flow, flexibility, and peace of mind, then now may be the perfect time—for you.