Personal loans can be helpful financial tools—but only when used correctly. Many Americans lose thousands of dollars due to avoidable mistakes like ignoring APRs, borrowing more than necessary, or choosing the wrong lender. This in-depth guide uncovers the most costly personal loan mistakes, real-life examples, and expert-backed strategies to help you borrow smarter, protect your credit, and avoid long-term financial regret.

Personal loans have become one of the fastest-growing forms of consumer debt in the United States. According to Experian, more than 23 million Americans currently carry a personal loan balance, with average balances rising steadily over the past few years.

On the surface, personal loans seem simple. Fixed interest rates. Predictable monthly payments. Clear payoff timelines. But beneath that simplicity lies a product that can quietly drain thousands of dollars from borrowers who don’t fully understand what they’re signing up for.

Unlike mortgages or auto loans, personal loans are often approved quickly, marketed aggressively, and taken without professional advice. That combination makes them especially risky for first-time borrowers.

What makes personal loans dangerous isn’t the product itself—it’s the mistakes people make before borrowing.

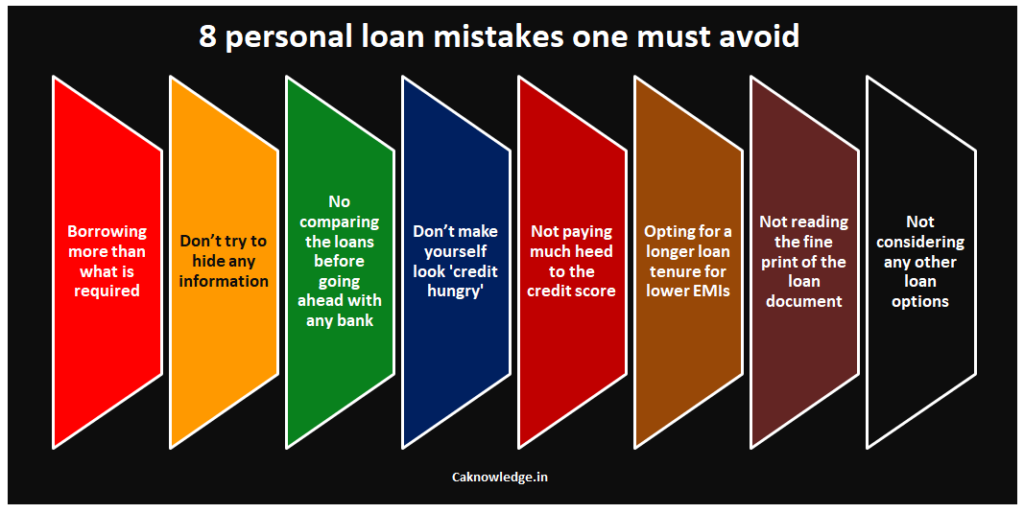

The biggest mistake borrowers make is assuming that approval equals affordability.

Just because a lender approves you for a loan doesn’t mean:

- It’s the cheapest option

- It’s the right amount

- It fits safely into your long-term budget

Lenders evaluate risk, not your future comfort. Their goal is repayment with interest—your goal should be minimizing cost and financial stress.

One of the most expensive errors borrowers make is focusing only on the monthly payment.

A lower monthly payment often means:

- A longer loan term

- More interest paid over time

- A higher total repayment amount

Jessica, a healthcare worker in Ohio, took a $15,000 personal loan to consolidate credit card debt. She chose a five-year term because the $340 monthly payment felt comfortable. What she didn’t realize was that her 18.9% APR would cost her nearly $6,000 in interest over the life of the loan.

Had she chosen a three-year term, she would have paid more each month—but saved thousands overall.

Many lenders encourage borrowers to take more than they need, framing it as a “financial cushion.” While it sounds helpful, it’s one of the easiest ways to overpay.

Every extra dollar borrowed accrues interest.

- Higher balances increase total interest

- Larger loans hurt debt-to-income ratios

- Extra funds often get spent unnecessarily

A homeowner approved for a $25,000 loan only needed $18,000 for repairs. The extra $7,000 ended up funding lifestyle purchases—and added more than $2,500 in interest over the loan term.

Many personal loans advertise “low interest rates” but quietly include fees that inflate the real cost.

Common fees include:

- Origination fees (typically 1%–8%)

- Late payment fees

- Returned payment penalties

- Administrative charges

According to the Consumer Financial Protection Bureau, origination fees alone can reduce the amount you receive by hundreds or even thousands of dollars upfront, while you still pay interest on the full loan amount.

Personal loan APRs can vary dramatically between lenders—even for the same borrower.

Credit unions, online lenders, and traditional banks all price risk differently. Failing to compare offers is one of the easiest ways to lose money.

A borrower with a 720 credit score received:

- 17.5% APR from a large bank

- 11.2% APR from a credit union

That difference saved over $4,000 on a $20,000 loan.

Personal loans are best used for strategic financial purposes, not lifestyle upgrades.

Higher-risk uses include:

- Vacations

- Luxury purchases

- Covering recurring expenses

- Gambling or speculative investments

Lower-risk, smarter uses include:

- High-interest debt consolidation

- Emergency expenses

- Medical bills

- Essential home repairs

Borrowing for non-essential spending often leads to regret once the excitement fades—but the payments remain.

Fixed payments don’t protect you from life changes.

Job loss, medical emergencies, inflation, or unexpected expenses can quickly turn a manageable payment into a financial burden.

During recent economic slowdowns, many borrowers found themselves locked into personal loan payments with no flexibility—damaging their credit when payments were missed.

Personal loans affect credit in several ways:

- Hard inquiries temporarily lower scores

- New accounts reduce average credit age

- High balances increase debt ratios

- Missed payments cause severe damage

Used responsibly, personal loans can improve credit. Used carelessly, they can undo years of progress.

Many borrowers take loans without answering one critical question:

“What if my income changes?”

Before borrowing, you should know:

- Whether you can prepay without penalties

- If refinancing is realistic

- How you’d manage payments during hardship

Loans without an exit plan often turn into long-term financial traps.

Before accepting any personal loan:

- Compare at least 3–5 lenders

- Calculate total repayment cost

- Choose the shortest affordable term

- Borrow only what you need

- Confirm all fees in writing

- Avoid prepayment penalties

- Ensure payments fit conservative income assumptions

Personal loan companies profit from:

- Higher interest paid over time

- Longer loan terms

- Origination and servicing fees

The more informed you are, the less profitable you become. That’s why borrower education is essential—and often missing from marketing materials.

1. Are personal loans a bad idea?

Ans. Personal loans are not inherently bad. They can be useful for consolidating high-interest debt or covering emergencies. Problems arise when borrowers ignore APRs, fees, or borrow for non-essential spending.

2. What is a good APR for a personal loan in the US?

Ans. Borrowers with excellent credit may qualify for APRs between 6% and 10%, while average credit borrowers often see rates between 11% and 20%.

3. Do personal loans hurt your credit score?

Ans. Initially, yes—due to hard credit inquiries. Over time, consistent on-time payments can improve your credit profile.

4. Is a personal loan better than a credit card?

Ans. Personal loans usually have lower interest rates than credit cards, making them better for large balances that need structured repayment.

5. Should I pay off my personal loan early?

Ans. Yes, if there is no prepayment penalty. Early payoff reduces interest costs and improves debt-to-income ratios.

6. How much personal loan debt is too much?

Ans. If your total monthly debt exceeds 36%–43% of your gross income, lenders generally consider it risky.

7. Can I refinance a personal loan later?

Ans. Yes, refinancing is possible if your credit and income improve, though new fees may apply.

8. Are online personal loan lenders safe?

Ans. Many are legitimate, but borrowers should verify licensing, read reviews, and ensure transparent disclosures.

9. What happens if I miss a personal loan payment?

Ans. Missed payments can result in fees, credit score damage, and potential collections activity.

10. What’s the smartest way to use a personal loan?

Ans. Using a personal loan to replace higher-interest debt with a clear payoff plan is generally the most strategic approach.

Personal loans aren’t dangerous because they exist—they’re dangerous when borrowers rush into them without understanding the real cost.

A few careful decisions before borrowing can mean the difference between saving money and losing thousands. Knowledge, comparison, and planning are your strongest tools.

Borrow wisely—and make the loan work for you, not against you.