As 2026 approaches, financial advisors agree that traditional money rules no longer work. Inflation, job volatility, rising healthcare costs, and market uncertainty demand smarter, faster financial decisions. This in-depth guide explains the seven essential money moves Americans must make before 2026—covering saving, debt, investing, income security, and protection—using real-life examples, 2026-era data, and practical steps you can apply immediately.

For decades, Americans followed a familiar financial script: save 10–15% of income, buy a home, invest steadily, and trust that things would work out over time. That script is breaking down.

According to data released by the Federal Reserve, household expenses tied to housing, healthcare, insurance, and debt servicing have risen faster than wages for most income brackets since 2021. By early 2026, many of these costs are expected to stabilize—but at permanently higher levels.

Financial advisors across the U.S. are aligned on one message:

2026 will reward people who adjusted early—and punish those who delayed.

This article is designed to answer the exact questions Americans are searching right now:

- What money moves should I make before 2026?

- How do I protect my finances from job loss or recession?

- Is saving 15% still enough?

- What do financial advisors actually recommend in 2026?

What follows is a ready-to-publish, long-form guide built for real people—not theory. Each money move is supported by advisor logic, real-life examples, and clear takeaways you can apply immediately.

For years, saving 10–15% of your income was considered responsible. In 2026, advisors increasingly view that number as financially dangerous, especially for anyone underprepared for retirement.

Research from Vanguard shows that Americans who began serious retirement saving after age 35 must save at least 20–25% of gross income to maintain their lifestyle in retirement—assuming moderate market returns and longer life expectancy.

Several structural shifts make higher savings unavoidable:

- Healthcare costs continue to outpace inflation

- People are living longer, extending retirement timelines

- Fewer employers offer pensions

- Market volatility reduces the reliability of returns

David, a 41-year-old operations manager in Ohio, saved 14% of his income for over a decade. When his advisor ran updated projections using 2026 assumptions—higher medical costs, slower growth, longer lifespan—David discovered he was on track to run out of money by age 79. Increasing his savings rate to 23% felt painful, but it restored long-term stability.

- Redirect raises, bonuses, and tax refunds automatically

- Increase savings by 1–2% every 90 days

- Automate transfers so you never “see” the money

Advisor takeaway: In 2026, savings rate matters more than chasing higher investment returns.

The traditional advice of a three- to six-month emergency fund was built for a different economy—one with stable jobs, predictable healthcare costs, and easier reemployment.

Data from the Bureau of Labor Statistics shows that average job search durations increased steadily through 2025, especially for mid- and senior-level professionals.

A full-year emergency fund protects you from:

- Prolonged layoffs or hiring freezes

- Career transitions driven by AI or automation

- Medical events with high deductibles

- Caregiving responsibilities for family members

- High-yield savings accounts

- Money market accounts

- Not invested in stocks or volatile assets

This fund isn’t about earning returns—it’s about buying time and peace of mind.

By early 2026, average U.S. credit card APRs remain above 20%. That means carrying high-interest debt silently destroys wealth faster than most investments can build it.

Financial advisors are increasingly unified around one rule:

Any debt above ~7% interest is an emergency.

Many households invest regularly while quietly carrying:

- Credit card balances

- Personal loans

- Stacked “buy now, pay later” obligations

This creates a false sense of progress while net worth stagnates.

- Starter emergency fund

- Pay off high-interest debt

- Capture employer retirement match

- Invest consistently

This sequence maximizes both financial security and long-term growth.

“How do I protect myself financially if I lose my job?”

Even high-income professionals are vulnerable. AI-driven restructuring has affected technology, marketing, finance, legal services, and healthcare administration.

It does not mean quitting your job. It means:

- Building one additional income stream

- Developing skills that can generate money independently

- Creating options before you need them

Jasmine, a marketing director in Chicago, began freelance consulting in 2023. When her company downsized in 2025, her side income covered 60% of expenses—giving her negotiation power and emotional stability.

Advisor takeaway: Income diversity is the new job security.

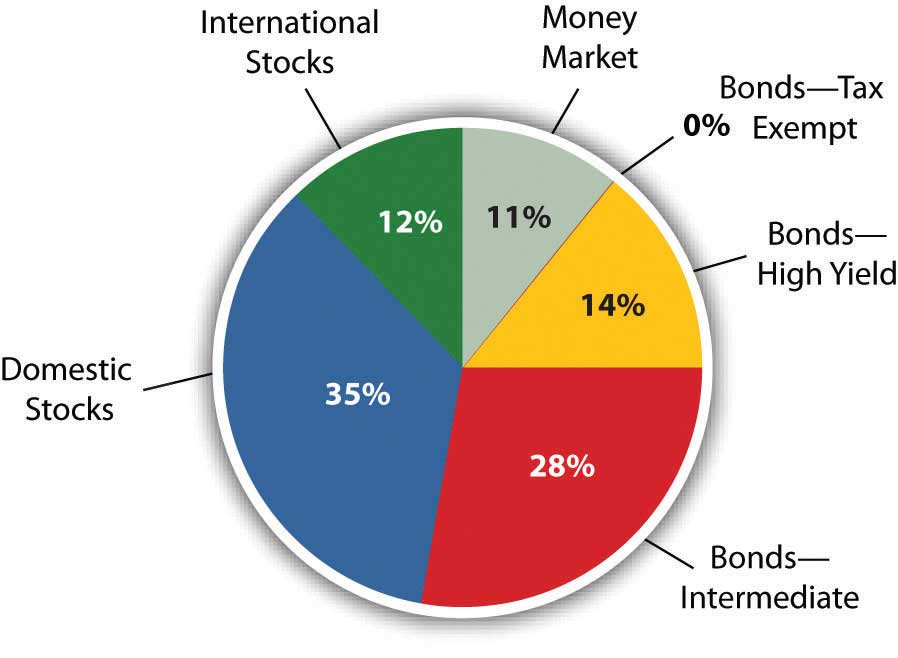

Markets in the 2020s have become faster, more emotional, and more sensitive to global events. Advisors warn that portfolios built purely for growth without resilience expose investors to unnecessary stress.

- Broader asset diversification

- Reduced concentration in individual stocks

- Attention to fees and tax efficiency

- Rebalancing aligned with risk tolerance

The goal in 2026 is not maximum returns—it’s durable progress through uncertainty.

Insurance is often ignored until something goes wrong. In 2026, advisors consider this one of the most overlooked money moves.

- Higher medical out-of-pocket maximums

- Climate-related property damage

- More freelance and contract work without employer benefits

- Health insurance deductibles

- Disability insurance (especially for high earners)

- Life insurance adequacy

- Umbrella liability coverage

Insurance isn’t pessimism—it’s financial shock absorption.

The final move is about control and clarity.

A fiduciary advisor is legally obligated to act in your best interest. Many Americans still receive commission-based advice without realizing it.

Organizations like the Certified Financial Planner Board emphasize disciplined planning, transparency, and long-term thinking heading into 2026.

- Learn basic tax planning

- Understand risk and asset allocation

- Review your plan annually—not emotionally

Most advisors recommend 20–25% of gross income, depending on age and goals.

For many households, 15% is no longer sufficient to offset higher future costs.

High-interest debt should usually be eliminated before aggressive investing.

Not in a volatile job market—advisors increasingly see it as necessary.

Not required, but income diversification dramatically reduces financial risk.

Yes—when approached with diversification and realistic expectations.

Not always, but fiduciary guidance adds clarity and discipline.

Waiting too long to update outdated money strategies.

At least once per year—or after major life changes.

Track spending honestly and increase your savings rate.

Financial advisors aren’t predicting disaster—they’re warning against inertia. The people who thrive financially in 2026 won’t necessarily earn more; they’ll adapt faster.

If you implement these seven money moves now, you’re not just improving numbers on a spreadsheet. You’re buying flexibility, confidence, and long-term freedom in an economy that rewards preparedness.