Mortgage refinancing can be a powerful financial move—but only when homeowners understand what lenders rarely explain. From hidden costs and misleading “low payment” offers to timing traps and rate markups, many refinances quietly favor banks over borrowers. This in-depth guide reveals the most important mortgage refinancing secrets, helping homeowners save money, avoid costly mistakes, and refinance with clarity and confidence.

Mortgage refinancing is often presented as a simple opportunity: lower your interest rate, reduce your monthly payment, and free up cash. But for many homeowners, refinancing ends with confusion, frustration, and regret.

The reason is simple—banks make significant profits from refinancing, and the process is structured to benefit lenders first. While refinancing can be a smart financial move, many borrowers unknowingly accept terms that increase long-term costs, reset loan timelines, or lock them into unfavorable structures.

According to Freddie Mac, homeowners who failed to compare multiple refinance offers paid thousands more over the life of their loans than those who shopped around. Yet most borrowers still refinance with the first lender they speak to.

This article uncovers the mortgage refinancing secrets banks don’t want you to know, explained clearly, without jargon, and supported by real-life examples—so you can make decisions that truly serve your financial future.

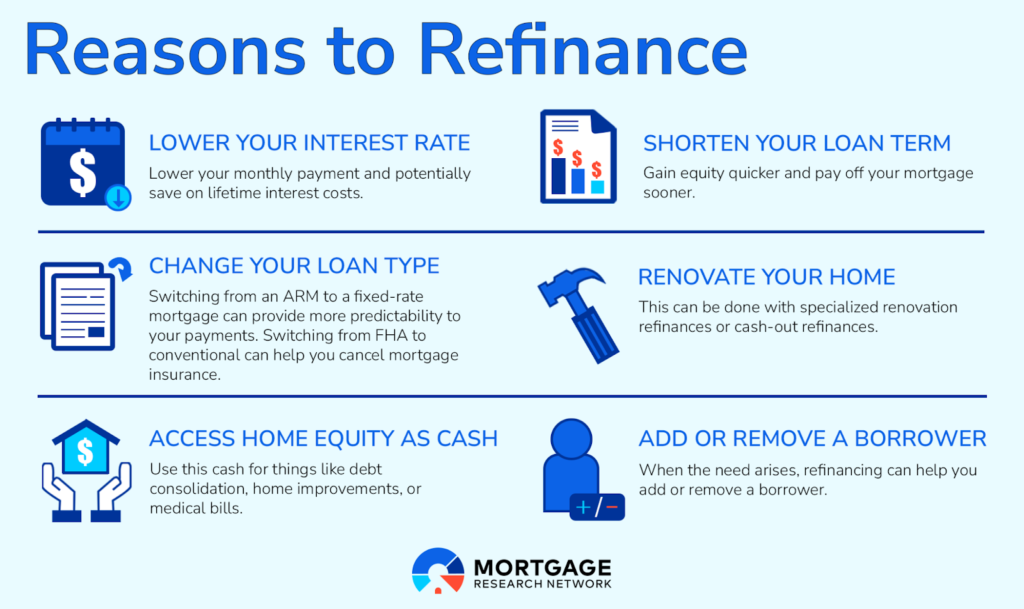

Mortgage refinancing replaces your current home loan with a new one. Homeowners typically refinance to:

- Secure a lower interest rate

- Reduce monthly payments

- Change loan terms

- Access home equity

- Switch from adjustable to fixed rates

Banks actively market refinancing because it generates:

- Origination fees

- Interest income over extended periods

- Opportunities to restructure loans in their favor

For homeowners, refinancing is neither good nor bad by default. The outcome depends entirely on structure, timing, and transparency—areas where banks are often vague.

One of the biggest refinancing traps is focusing only on the monthly payment.

Banks frequently lower payments by resetting the loan to a new 30-year term, even if you’ve already paid off years of your mortgage. While the payment looks attractive, the total interest paid often skyrockets.

Real-life example:

A homeowner in Ohio refinanced after eight years of payments and reduced his monthly bill by $310. What the lender didn’t emphasize was that restarting a 30-year loan added nearly $70,000 in additional interest over time.

Lower payments feel good now—but long-term costs matter more.

Many homeowners assume refinancing rates depend mostly on credit scores. While credit is important, lenders also evaluate:

- Loan-to-value (LTV) ratio

- Debt-to-income (DTI) ratio

- Property type

- Occupancy status

- Market conditions and profit margins

A borrower in Arizona with excellent credit received rates ranging from 6.1% to 6.9%—simply because lenders priced risk differently.

The lesson? Rates are negotiable, and comparison is essential.

Banks often advertise no-closing-cost refinancing to remove psychological barriers. In reality, those costs don’t disappear—they’re just shifted.

Usually, lenders:

- Raise the interest rate

- Roll fees into the loan balance

According to the Consumer Financial Protection Bureau (CFPB), homeowners who keep these loans longer than five years often pay significantly more than if they had paid closing costs upfront.

No-closing-cost options can make sense—but only when aligned with short-term plans.

Banks benefit when homeowners refinance impulsively based on headlines like “Rates Just Dropped!”

Smart refinancing considers:

- How long you’ll stay in the home

- Break-even timelines

- Future rate trends

- Life plans (relocation, retirement, income changes)

A couple in North Carolina refinanced during a rate dip but sold their home three years later—never recouping closing costs.

The best refinance is the one that fits your timeline, not market hype.

Your first refinance quote is almost never the best available.

Banks assume:

- Borrowers won’t shop around

- Convenience will override savings

- Confusion reduces negotiation

Freddie Mac data shows homeowners who request at least three quotes save an average of $3,000 to $5,000 over the life of the loan.

Comparison isn’t optional—it’s essential.

Cash-out refinancing allows homeowners to tap into home equity, often marketed as “smart leverage.” But banks rarely emphasize the downside.

Risks include:

- Higher interest rates

- Larger loan balances

- Extended payoff timelines

- Reduced financial safety cushion

A California homeowner used cash-out refinancing for renovations, only to face financial stress when property values temporarily dipped.

Cash-out refinancing should be strategic—not emotional.

Banks often default to offering 30-year refinances, even when borrowers qualify for shorter terms.

Switching to a 15- or 20-year refinance can:

- Cut total interest dramatically

- Build equity faster

- Improve long-term financial security

A Texas homeowner refinanced into a 20-year loan instead of restarting a 30-year term and saved over $90,000 in interest.

Shorter terms aren’t just for high earners—they’re for informed borrowers.

Banks rarely explain how much influence appraisals have during refinancing.

A low appraisal can:

- Increase interest rates

- Reintroduce PMI

- Disqualify refinancing altogether

Some borrowers qualify for appraisal waivers—but lenders don’t always mention them unless asked.

Knowing your home’s current market value before applying gives you leverage.

Some homeowners refinance every time rates drop slightly. While this feels proactive, it often results in:

- Repeated closing costs

- Constant loan resets

- Minimal net benefit

A Florida homeowner refinanced four times in seven years and later realized she barely shortened her payoff timeline.

Refinancing should be intentional—not habitual.

Many homeowners assume their current lender will reward loyalty. In reality, banks often reserve the best rates for new customers.

Borrowers who shop aggressively almost always receive better terms than those who stay loyal out of convenience.

Mortgage refinancing is a marketplace—treat it like one.

Before refinancing, homeowners should:

- Calculate break-even points

- Compare 3–5 lenders

- Request full loan estimates

- Align refinancing with long-term goals

The smartest refinances are driven by strategy, not emotion.

Many refinancing regrets stem from:

- Focusing only on monthly payment

- Ignoring total interest paid

- Not reading loan estimates carefully

- Refinancing without a clear objective

Avoiding these mistakes often saves more than chasing the lowest advertised rate.

1. What is the biggest secret banks hide about mortgage refinancing?

Ans. Banks often downplay how restarting a loan term significantly increases total interest paid over time.

2. How many refinance quotes should I get?

Ans. At least three to five quotes to ensure competitive rates and lower fees.

3. Is refinancing always smart when rates fall?

Ans. No. Refinancing only makes sense if you reach your break-even point before selling or refinancing again.

4. Are no-closing-cost refinances a good idea?

Ans. They can be, but only if you plan to move or refinance again within a short period.

5. Does refinancing hurt your credit score?

Ans. There may be a small, temporary dip, but it usually recovers quickly.

6. How often should homeowners refinance?

Ans. Only when it aligns with long-term financial goals—not just minor rate changes.

7. Is cash-out refinancing risky?

Ans. Yes, if it increases debt without improving long-term financial stability.

8. Can I refinance with low equity?

Ans. It depends on loan type, credit profile, and current market conditions.

9. Should I refinance with my current lender?

Ans. You can, but you should still compare outside offers to ensure competitive terms.

10. What is the smartest reason to refinance a mortgage?

Ans. To reduce total interest paid and align your loan with long-term financial goals.