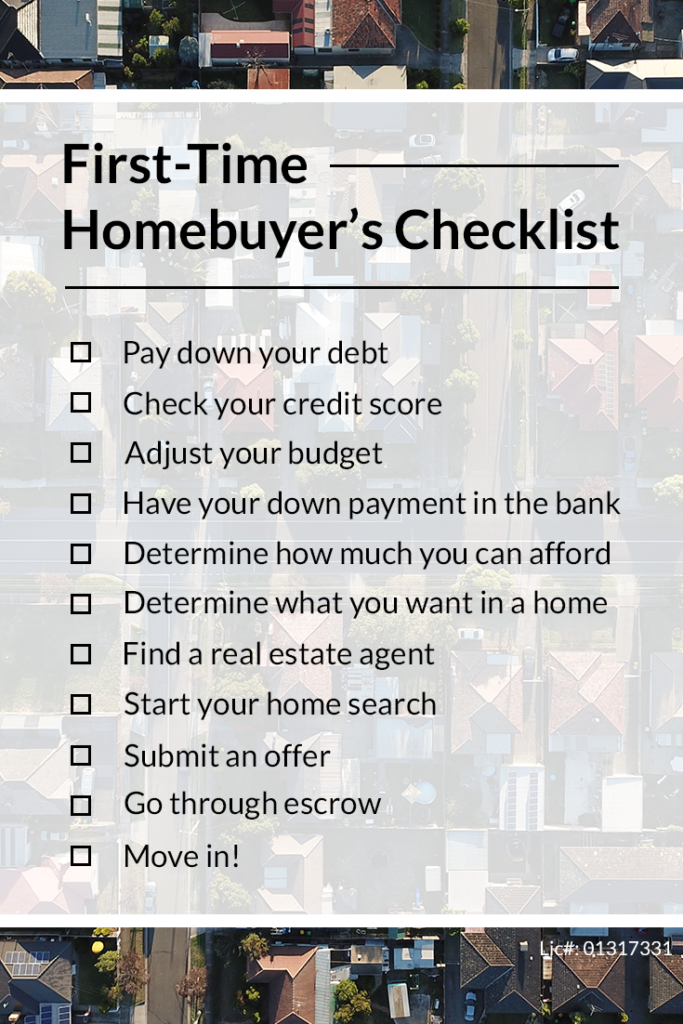

Moving from renting to owning a home is a major financial and emotional shift. Many first-time buyers feel overwhelmed because they lack a clear roadmap. This comprehensive guide breaks down the entire journey—from preparing finances and improving credit to choosing the right home and managing life after closing—using real-life examples and expert insights to help renters become confident homeowners without costly mistakes.

For years, renting feels predictable. You pay rent, call the landlord when something breaks, and move on with life. But over time, rising rents, limited control, and the feeling of “throwing money away” push many Americans toward homeownership.

Yet when renters finally decide to buy, confusion sets in.

According to the National Association of Realtors, more than 60% of first-time buyers say the process felt more stressful than expected. They aren’t confused because they’re careless—they’re confused because most advice skips steps, assumes prior knowledge, or jumps straight to house hunting without proper preparation.

What first-time buyers really need is a step-by-step blueprint that explains what to do, when to do it, and why it matters. This guide provides exactly that.

One of the biggest myths is that buying a home is something you do when you reach a certain age or life stage. In reality, readiness is about financial and lifestyle stability, not timing the market.

A renter in Seattle felt pressured to buy because friends were purchasing homes. After reviewing her finances, she realized her job situation was unstable. She waited another year, built savings, and later bought with far less stress and better loan terms.

You may be ready to buy if:

- Your income is stable and predictable

- You plan to stay in the same area for several years

- You can afford ownership without sacrificing essentials

Buying too early often creates regret. Buying prepared creates confidence.

Many renters assume that whatever amount a lender approves is what they should spend. This is one of the most expensive misunderstandings in homeownership.

Lenders calculate approval based on formulas—not on your lifestyle.

A buyer in Florida was approved for $500,000 but chose a $385,000 home instead. As a result:

- Monthly finances felt manageable

- Savings continued after closing

- Financial stress stayed low

True affordability includes:

- Mortgage payments

- Property taxes

- Insurance

- Maintenance

- Utilities and repairs

A comfortable home payment supports your life—it doesn’t dominate it.

Renters often underestimate how different owning feels financially. The smartest buyers “practice” ownership before buying.

This means:

- Saving the difference between rent and estimated mortgage

- Planning for higher utilities

- Setting aside money for maintenance

If you can live comfortably on your future homeowner budget now, ownership will feel far less overwhelming later.

Credit doesn’t just determine approval—it determines cost.

According to the Consumer Financial Protection Bureau, even a small improvement in credit score can save buyers tens of thousands of dollars in interest over the life of a loan.

Two buyers with similar incomes applied for mortgages:

- Buyer A had a 760 credit score

- Buyer B had a 680 credit score

Buyer A received a significantly lower interest rate and saved over $40,000 long-term.

Before buying:

- Pay down credit card balances

- Avoid new debt

- Make all payments on time

Credit preparation is one of the highest-impact steps you can take.

Many renters delay buying because they believe 20% down is required. In reality, many first-time buyers purchase with much less.

Common options include:

- 3–5% down payments

- First-time buyer programs

- Down payment assistance

What matters just as much as the down payment:

- Closing costs

- Emergency savings

- Post-purchase cash buffer

Savings create flexibility—and flexibility reduces stress.

Mortgages are not one-size-fits-all. The best loan is the one that matches your timeline, risk tolerance, and income stability.

Smart buyers:

- Compare multiple lenders

- Understand loan structures

- Focus on long-term affordability

Choosing the right loan can matter more than timing the market.

House hunting without clarity often leads to emotional decisions.

Successful buyers define:

- Non-negotiable features

- Nice-to-have upgrades

- Clear walk-away limits

A buyer in Atlanta avoided bidding wars by sticking to her criteria. Weeks later, she found a better home at a fair price.

Clarity protects you from pressure.

Overpaying doesn’t just affect today—it impacts resale and long-term wealth.

Buyers avoid overpaying by:

- Reviewing comparable recent sales

- Understanding neighborhood trends

- Keeping emotion out of offers

A good home should also be a good financial decision.

Many first-time buyers feel anxious after their offer is accepted. This phase is where due diligence protects you.

Key steps include:

- Home inspection

- Appraisal

- Final loan approval

An inspection revealed major plumbing issues. The buyer negotiated credits and avoided future debt.

This stage exists to protect buyers—use it fully.

Closing day isn’t the finish line—it’s the transition point.

New homeowners experience:

- Maintenance responsibilities

- Lifestyle cost increases

- A learning curve

Planning for this phase prevents financial surprises and stress.

- Buying at the top of their approval range

- Rushing due to fear of missing out

- Skipping inspections

- Underestimating ownership costs

- Ignoring future flexibility

Avoiding mistakes matters more than buying fast.

- Preparation beats urgency

- Comfort matters more than approval

- Systems reduce stress

- Ownership should add stability, not pressure

- A clear plan prevents regret

Ans.

Buying makes sense when income is stable, you plan to stay put for several years, and ownership fits comfortably within your budget.

Ans.

Many first-time buyers purchase with 3–5% down, plus savings for closing costs and emergencies.

Ans.

The best time to buy is when your finances are ready, not when the market feels perfect.

Ans.

Some loans allow scores in the mid-600s, but higher scores significantly reduce long-term costs.

Ans.

Yes. Many first-time buyers succeed through disciplined saving and assistance programs.

Ans.

Buying more house than they can comfortably afford based on lender approval.

Ans.

With preparation, many renters become homeowners within 1–3 years.

Ans.

Yes. They can reduce upfront costs and improve affordability when used correctly.

Ans.

Maintenance, repairs, utilities, and post-purchase lifestyle expenses.

Ans.

By following a step-by-step plan, staying within budget, and making data-driven decisions.

Most renters don’t struggle to become homeowners because they lack money. They struggle because they lack clarity.

When you understand each step—from financial readiness to life after closing—the process becomes manageable instead of intimidating. Homeownership isn’t about rushing. It’s about preparing intelligently.

This blueprint doesn’t promise shortcuts.

It delivers confidence, control, and long-term stability—exactly what first-time buyers wish they had sooner.